Robust, but not immune

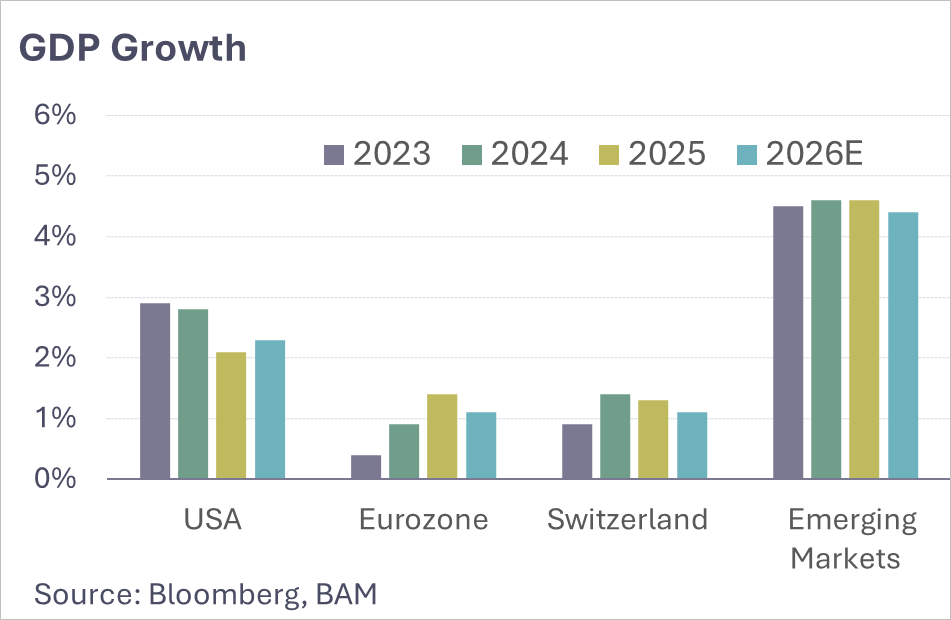

The global economy remains resilient despite an environment shaped increasingly by geopolitical tensions. Growth is stable, yet uncertainties are clearly rising. In the United States, momentum remains solid. The labour market is showing initial signs of cooling, but continues to be supportive. Growth is increasingly driven by investment, particularly in technology-driven sectors. The recent rise in energy prices is inflationary, but likely temporary, leaving monetary policy in a wait-and-see stance for now.

Europe remains heterogeneous and structurally challenged. Dependence on energy imports continues to increase vulnerability to external shocks, although there are growing signs of stabilisation in the industrial sector. Fiscal stimulus, particularly in infrastructure and defence, are beginning to take effect, albeit unevenly across regions.

Emerging markets appear broadly more robust. Asia in particular benefits from structural trends such as the reconfiguration of global supply chains and continued investment in technology. These developments generate additional growth momentum, even if energy prices and transport disruptions create localised pressures.

Switzerland continues to act as a stable anchor. A solid domestic economy and internationally competitive companies underpin performance. The strong Swiss franc acts both as a stabiliser and a headwind for export-oriented sectors.

Overall, the picture is differentiated: the economy is intact but increasingly uneven, with clear regional differences and heightened sensitivity to external influences.