Structural pressure at the long end

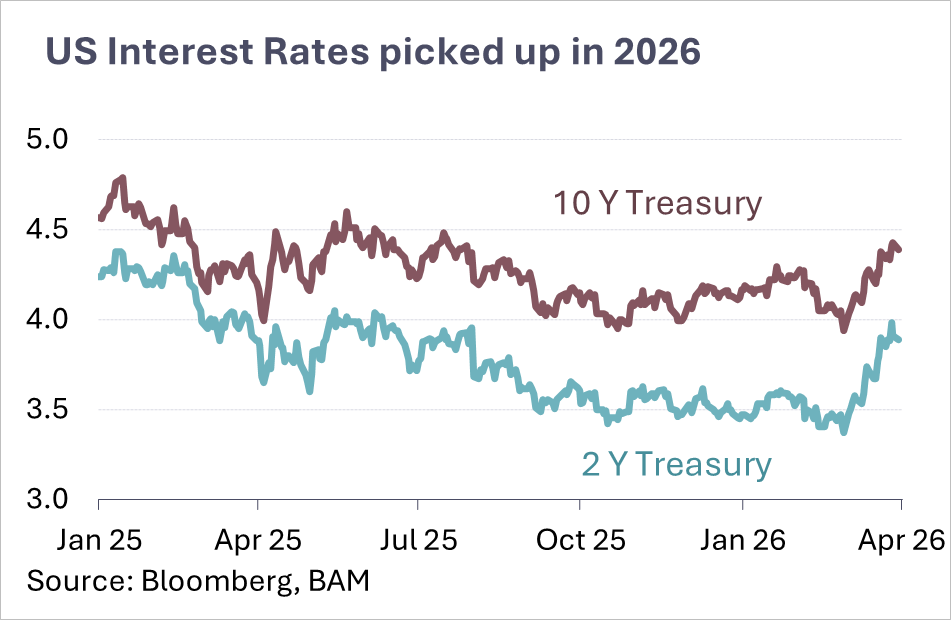

In the United States, monetary policy remains on hold. Inflation is not yet clearly converging towards its target of 2%. At the same time, the economy is robust enough to allow for further delays to rate cuts. Expectations of rapid easing have therefore moderated.

Additional uncertainty arises from the upcoming change at the helm of the Federal Reserve in May. While continuity is expected, subtle shifts may emerge in a challenging environment. Notably, developments at the long end of the yield curve are striking. US government bonds are under structural pressure, with investors demanding higher risk premia. Rising government debt and high issuance volumes are met with more cautious demand. As a result, long-term yields remain elevated despite declining inflation.

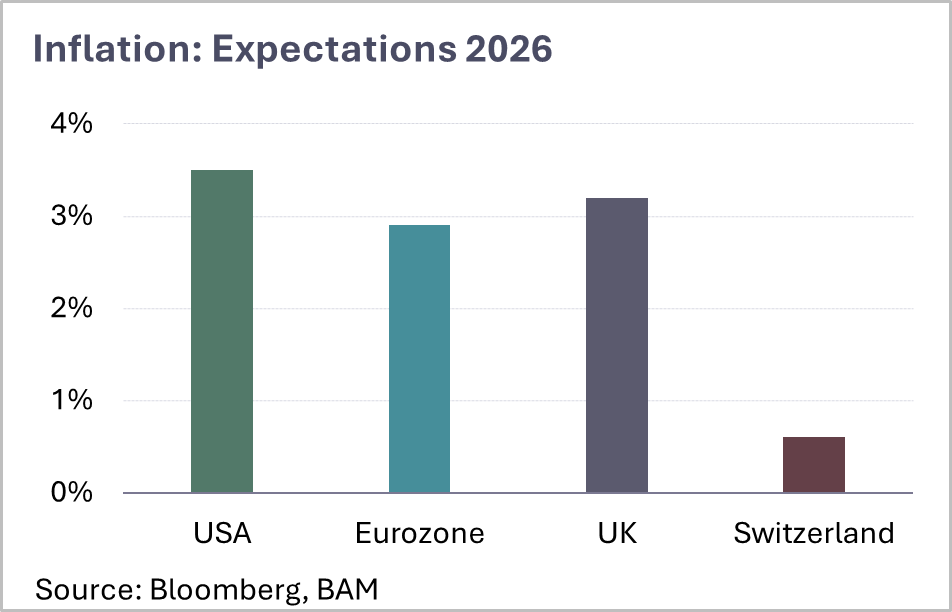

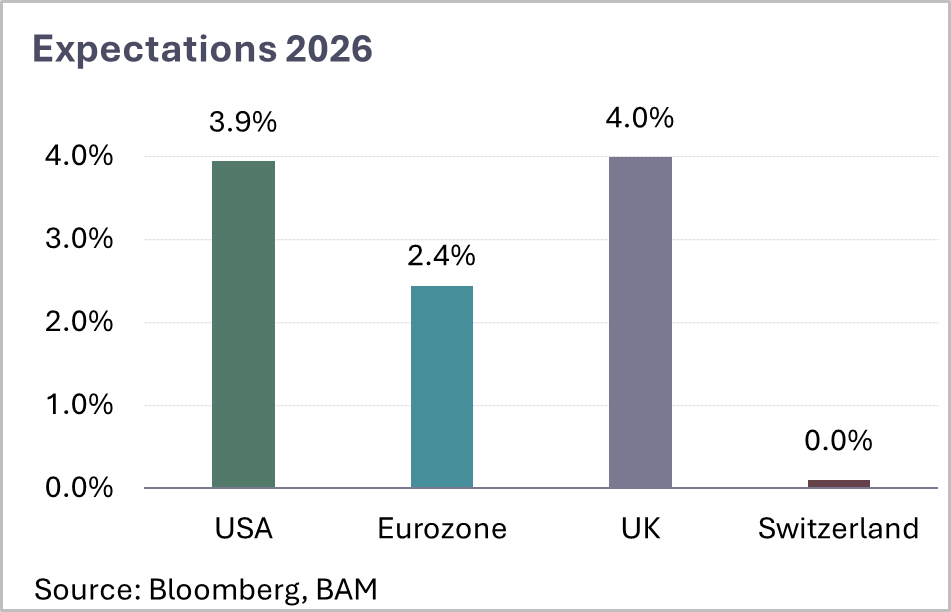

In Europe, monetary policy remains cautious. Inflation is now elevated, but weak economic growth limits the room to manoeuvre. Central banks are therefore acting in a restrained, data-dependent manner. Switzerland faces a different challenge. The Swiss franc is strengthening, putting pressure on the SNB. In the short term, foreign exchange interventions are likely the solution; in the medium term, further easing steps – including negative interest rates – remain a realistic outcome. Credit markets are also undergoing adjustment. Risk spreads on corporate bonds have widened, bringing quality and creditworthiness back into focus.

For investors, this implies increased caution regarding longer maturities. More attractive opportunities lie in selectively chosen corporate bonds with solid credit quality and shorter durations.