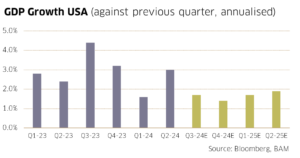

The US economy grew by a solid 3% in the second quarter. This pace is unlikely to be maintained in the second half of the year, lacking positive impulses. Unemployment is continuously rising and the Purchasing Managers’ Index shows that manufacturing is weakening.

Moreover, the government’s fiscal stimulus is drying up. However, there are factors that speak against a sharp slowdown or even a recession – such as a robust financial situation of private households, the decline in inflation, including cheaper petrol, and interest rate cuts, which lead to lower mortgages rates.

At the end of September, the Chinese government responded to the ailing real estate market with some new stabilising measures. These included lowering interest rates, easing mortgage repayments and injecting capital into six large state-owned banks. These measures might have a mildly positive effect, but are not likely to solve the fundamental problem that many private individuals have lost a lot of money with real estate investments.

The economic outlook for the eurozone has darkened further. The Purchasing Managers’ Index (PMI) for manufacturing fell by one point to a low 44.8 in September. The services sector, which had previously performed better, also lost momentum recently and the respective PMI noted barely above the expansion mark at 50.5 points. With this data, the economy is unlikely to grow much more by the end of the year. All hopes are pinned now on consumers, whose purchasing power is likely to increase thanks to lower inflation.

Equity markets got off to a similarly poor start in September as they did in August. Yet, the central banks’ interest rate cuts and new stimulus programs from the Chinese government gave equities a bit of a boost over the course of the month.

Overall, most stock markets performed slightly positively in September. The Euro Stoxx and the S&P 500 gained 2.3% and 1.7%, respectively. However, the SPI was unable to keep up with a performance of -1.1%, as the stocks of all three heavyweights ended with a loss. Small and medium-sized companies performed better, though, recording a gain of nearly 1% in September.

Equity markets are likely to remain volatile up to the US presidential elections on 5th November. It cannot be ruled out that new trade restrictions against China will be announced again for tactical reasons. However, we do not expect a major market decline because the prospect of interest rate cuts will have a supporting effect.