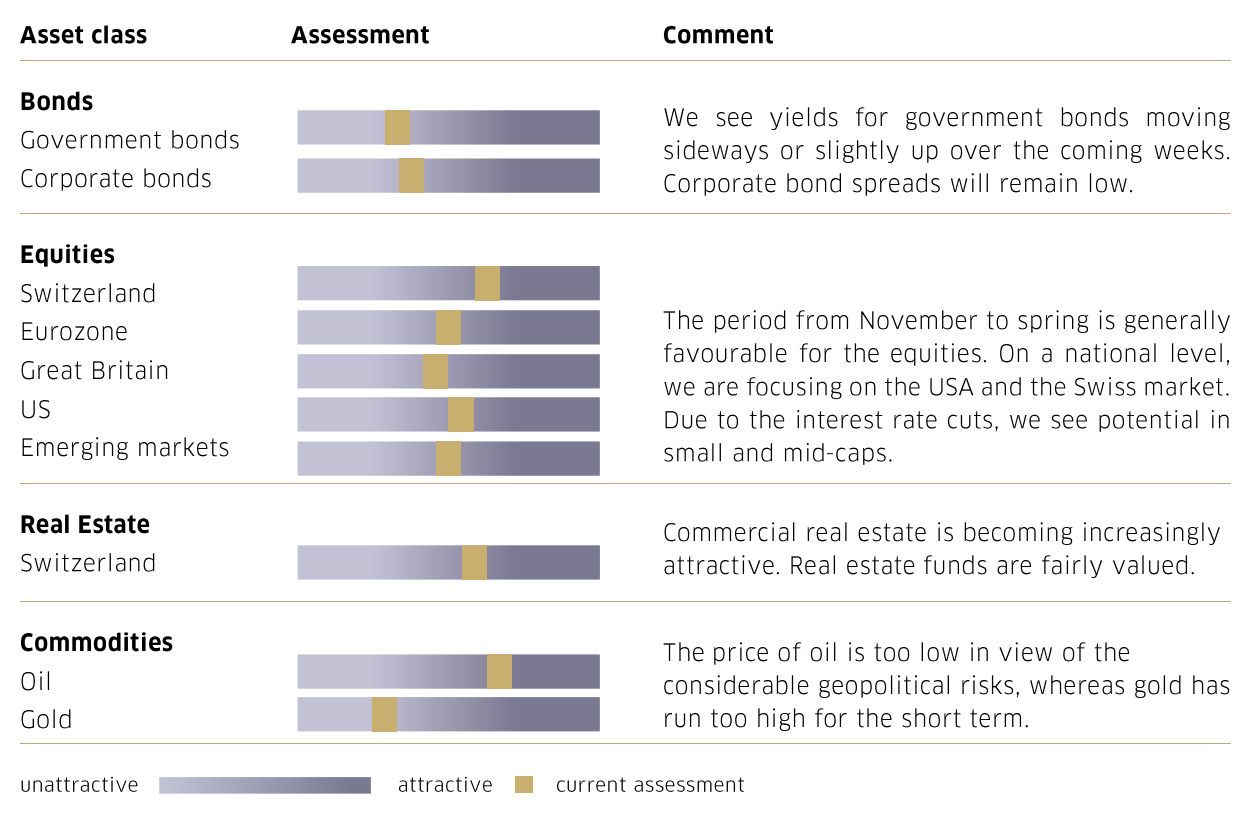

The US economy remained on a solid growth path in the third quarter. Supported by private consumption, GDP grew by an annualized 2.8% compared to the previous quarter. The labour market recovered significantly after a short-term weakness in September and is now a key driver for the strong consumption. Overall, the US economy is still the best performing of the three major global regions.

The Chinese government expanded its stimulus measures in October. However, market observers agree that they are still not sufficient to stabilize the real estate market. More public funds would be needed to destock the real estate market meaningfully and scale up social spending for the lower-income segments of the population. All in all, the challenges are still abundant, and the risk of a deflationary spiral persists.

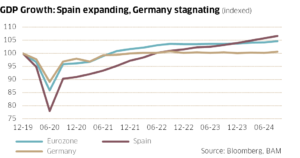

For once, economic figures in the eurozone surprised on the upside. GDP rose by 0.4% in the third quarter, which was above the expected 0.2%. The area benefited from a general recovery in private consumption and – on a national level – Spain with an above-average growth of 0.8%. Nevertheless, the euro zone is still facing significant challenges. These include notably weak foreign demand and new trade restrictions. Nevertheless, the labour market should remain quite solid, and the interest rate cuts ought to help in the medium term.

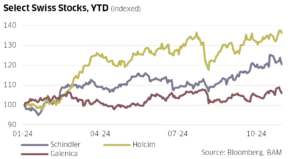

Equity market performance was mixed in October. In the US, the market benefited from the strong economy and overall better-than-expected third quarter earnings reports. One example is Netflix (+6.3% in October) with a significant increase in profitability. The S&P 500 and the Nasdaq rose by +1.0% and +2.3%, respectively in October. By contrast, Euro Stoxx and the SPI proved to be struggling, with month-on-month declines of -2.2% and -1.9%. The blue chips Novartis and Nestlé weighed on the performance of the SPI. Nestlé is contending with some growth and innovation issues that are unlikely to be resolved any time soon. However, there were also some bright spots, such as Holcim (+4.1%), Schindler (+2.0%) and Galenica (+1.9%). Holcim achieved a further increase in margins in the third quarter and the planned listing of its North American business is expected to generate additional shareholder value.

Now that the difficult months of September and October are behind us, there are good chances that equity markets could be in for a favourable run towards the year-end. The key drivers are good corporate earnings from the USA, further easing on the inflation front, interest rate cuts by central banks, and the Chinese government’s willingness to support the economy.