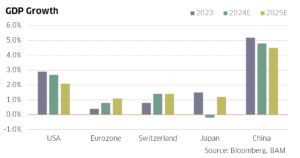

The usual picture did not change much in December. The US economy continues to perform well, almost too well. Therefore, there is a risk that inflation – currently at 3.3% (core rate) – will no longer make any notable progress towards the 2% mark. Hence, the Fed adopted a more cautious stance at its last meeting (see details below in INTEREST RATES). Moderate growth of around 2% is expected for the economy overall.

Meanwhile, the eurozone still faces significant challenges, the core culprit being Germany, where the economy has been stagnating since 2019. After Chancellor Scholz lost the vote of confidence, new elections are scheduled for 23rd February. Economic issues dominate the agenda and most parties are calling for tax cuts, lower energy prices and a reform of the citizens’ benefits (i.e., income support for job seekers) as an incentive to find employment again. Such reforms are desperately needed to get the economy moving and make Germany competitive again.

Although China’s export engine is running smoothly and making life difficult for Germany, among others, domestic demand remains weak due to the ongoing real estate crisis. The measures implemented by the government have led to a temporary increase in house sales, but construction activity remains significantly sub-dued. After a brief rebound in October, private consumption weakened again in November. The government will need to intensify efforts to achieve its growth target of 5% in 2025.

Led by US technology stocks, equity markets initially trended upwards in December. While most investors thought they were already on Christmas leave, Fed Chairman Jerome Powell shocked the markets on 18th December with the prospect of fewer interest rate cuts than expected. The S&P 500 reacted with a slump of 3%. Equity markets in Europe did not escape unscathed either, but their losses were less dramatic. Overall, the following performances were recorded in December: S&P 500: -2.0%, Euro Stoxx: +0.9% and SPI: -1.3%.

In the Swiss market, winning stocks were few and far between in December. Yet, there were some, for instance Richemont (+12.4%), which held its own in the luxury goods market. Swatch (+3.2%), however, faced challenges due to its focus on the mass market.

Equity markets should benefit from the January effect at the start of the year, which usually propels share prices upward. We expect a continuation of last year’s trends, which means a good performance of US equities. It will remain to be seen over the course of the year whether the other equity markets can break the spell of negative earnings momentum. The stronger US dollar provides a welcome tailwind, especially for Swiss companies.